Jacki Ellis We know from talking with our members that the key challenge when trying to plan for your retirement is just to know where to start or even how to begin to approach the complexity.

Geoff Kaye People have this belief that they've been putting into super all their lives. It's going to be enough not to have to worry about. It'll look after itself. And so they tend to sort of just keep putting it off and be a little bit complacent around their superannuation.

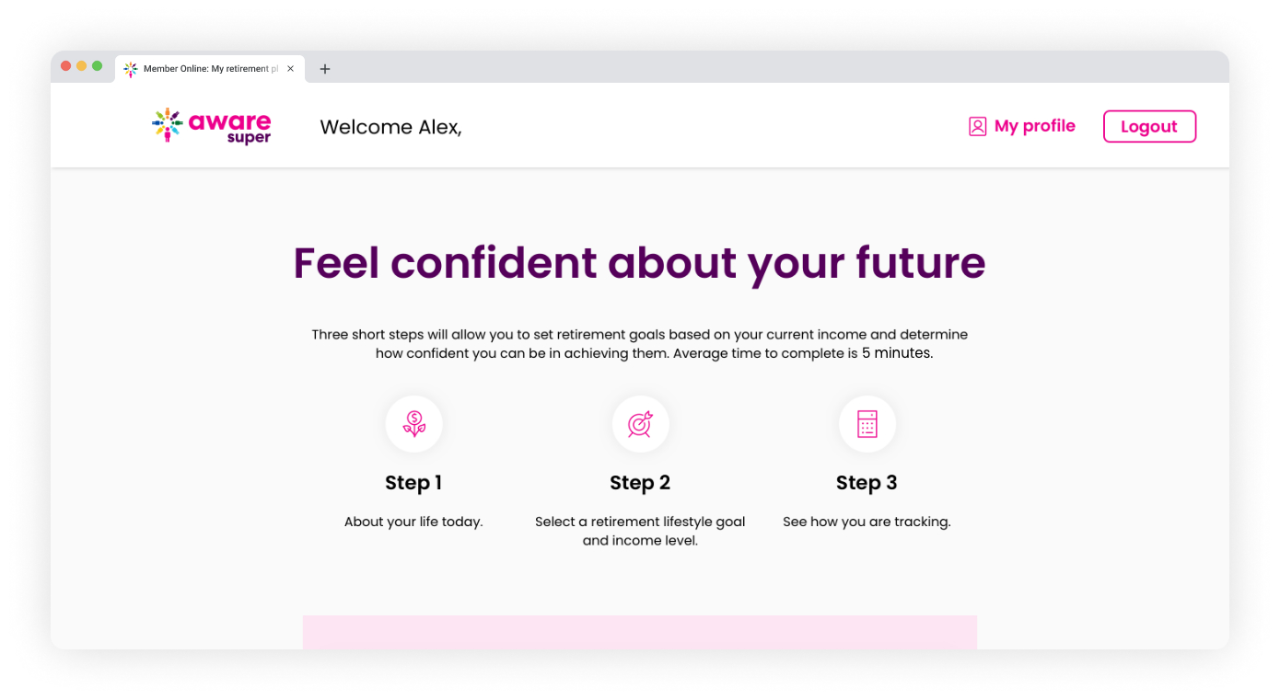

Jacki Ellis It's just so easy to put off things like retirement planning. But the great irony is that the best thing that you can do to support your lifestyle in retirement is actually to make that plan and know where you stand. We're here to help our members get set up for success. We know that helping them understand their circumstances, their goals and make a plan that works for them is really what's going to make a difference to their future retirement. So we have created my retirement plan, which is a easy to access, easy to use retirement calculator that's available to our Aware Super members. We've set up the tool to make it as super easy as possible to use, it's pre-populated with all the information we already know about you. Then you're guided through choices around the lifestyle that you're looking for in retirement. How much income do I need in retirement to maintain the lifestyle I know and love today? How on track am I to reach that goal and what can I do to get myself in even better shape for my future? So in the final step, you'll see how you're tracking towards your goals and also receive your retirement confidence score. We all know that we can't predict the future and markets go up and down. And so the retirement confidence score helps you understand how confident you can be that you're actually going to receive that estimate of what you'll get in retirement. And then you receive a detailed step by step plan so it's easy for you to know what to do next.

Geoff Kaye So for something that's quite sophisticated, it's actually very intuitive. And one of the great features is you can change various inputs to get a different outcome in a different answer and see how changing, whether it be your investment profile or your living expense needs, play around with those different fields to get a different outcome and see which decisions make the biggest impact on the long term outcome. You can organise to make an appointment, whether it be via the phone or video or face to face. Learn a bit more about how it all works and how it can get you on the right pathway.